Whole Life Companies & How to Choose Them

The wealthy use permanent insurance as ASSETS, here's how...

This is a post from my friend, contributor, and partner, Chris Robinette.

You can find this post (and more like these) in the Levels of Wealth resourcegroup. To read more of Chris’ work, go here.

Hey folks,

I have been receiving a lot of questions on whole life insurance types and want to look at beyond term insurance, so I wanted to give you part of my philosophy of what we talk to clients about in the financial planning process, and give you some ammunition to take back to your financial advisor and insurance agent to help you make the right decisions on what is best for you and your situation.

The odds are, I don't know the ins and outs of your situation, so please just take this as a framework to begin your research and study from, and feel free to ask the several competent and qualified life insurance folks in the resource group for guidance as well.

(ALSO, I did not create this list, I pulled it from topwholelife .com website, which is a great resource to see comparisons and breakdowns of companies)

The first thing we talk about in the planning process around life insurance is how much death benefit does a client need to have. This varies around needs and wants, and Dave Ramsey says this number should be 8-12x your income.

Based on your age you can build a risk pool in term insurance up to 35x your income. This could be important if you are in a career that is increasing your income each year, and you would rather over cover your coverage now instead of having to take new medical exams every 12 months to apply for and requalify each time. The younger and healthier you are, the better the rating you will tend to receive.

Once we have established what that your rating is in term insurance, that is when we will go look at how much discretionary income you have in your life to contribute towards building out a permanent policy.

My preference is to do a whole life policy as the policy of choice, and there are other options such as IUL and VUL that you can explore as well. I will focus on whole life for this discussion.

Whole life carriers are broken down between stock companies and mutual companies. A stock company is just like it sounds, and the shareholders of the company are not necessarily policyholders. A Mutual company all of the policyholders are the shareholders.

Why this is important distinction, is that when a company goes to pay a dividend, it will go to the shareholders first. A stock company therefore, will not necessarily pay anything to a policy holder, whereas a mutual company has to pay to the policyholder since they are the shareholder. I prefer my clients to work with mutual companies for their permanent insurance policies.

Inside of that there is then direct recognition and non-direct recognition. This refers to how you pull money out of the policy. While accumulation through the different types is essentially the same, the distribution is not.

A direct recognition company operates like a bank account. If there is money in the account, the dividend pays on that amount. If you take a loan or borrow from the policy, the amount of cash on hand goes down thus your dividend payout also reduces.

An non-direct recognition company operates more like a HELOC, and you take a loan against the policy. Thus you are borrowing against your cash value, yet the dividends are still being paid annually to the policy as if all of the funds are still in the policy. I find this to be more beneficial for clients when utilizing their policies for loans for projects or as a retirement supplement for their future etc.

I have attached a list of major direct and non direct recognition companies for you to reference.

Direct Recognition

Ameritas, Country Financial, Massmutual*, Minnesota Life, Mutual Trust Life, Northwestern Mutual, Penn Mutual, Savings Bank Life of Massachusetts , Security Mutual, The Guardian, Thrivent

Non- Direct Recognition

Ohio National, New York Life, MassMutual*, MetLife, Lafayette Life Foresters

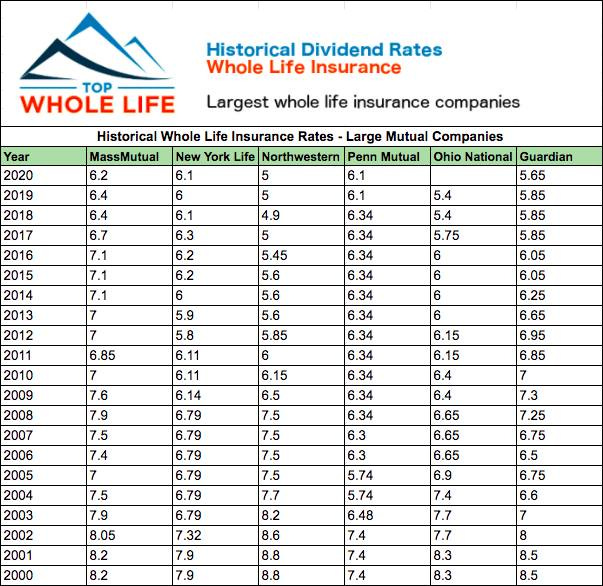

Finally, new guidance is coming out for 2022 dividend scales from companies, and this is as up to date as I have been able to gather so far. This should give you a decent idea of what the policy should be generating on their non-guaranteed dividend for next year. I also attached two photos so you can see the dividend average of these companies, and also the historic year to year breakdown as well for reference.

MassMutual 6.0

Penn Mutual 5.75

New York Life 5.80

Guardian Life 5.65

Foresters (No 2021 yet, 5.8% last year)

Northwestern Mutual 5.0

I hope that this has been beneficial for you as you continue to look at the next steps of building and growing your legacy. Again I would recommend you consult your financial planner/insurance agent to determine what type of and build of policy is right for you and your situation.

Hope you enjoyed this breakdown. If you’d like to speak with Chris about your situation you may do so here.

By the way - episode 2 of the brand new “Taylor Welch” YouTube has dropped… this is a behind the scenes into some trips, travels, meetings & shenanigans that will be 80% entertaining and 100% helpful.

More Resources: